By Andy Xie, guest economist to Caijing and board member of Rosetta Stone Advisors Limited

By Andy Xie, guest economist to Caijing and board member of Rosetta Stone Advisors LimitedChina has entered another era of inflation. It will last until the economy experiences a downturn like in 1997-98. The downturn could happen in three scenarios. First, inflation could get out of control and cause emergency braking in macro policy. Second, the global economy collapses and China's exports experience a severe downturn. Third, production capacity keeps growing faster than aggregate demand and overcapacity-led deflation ensues. China's macro policy should minimize the likelihood of all three scenarios and extend the growth cycle as long as possible.

Since the reform policy began in 1978, China was inflationary until 1994. The main reason was that China 's production capability was insufficient due to decades of poor economic management. The inflation made China less competitive in trade, and China resorted to devaluation to maintain competitiveness. But, devaluation made the economy more inflation-prone. The inflation-devaluation dynamic continued until 1994, and Yuan/Dollar exchange rate depreciated from 1.5 to 8.9 or by 83%. The inflation, however, taxed savers and funded investment.

China entered a deflationary period from 1994-2004. China had already built up enormous production capacity, partly funded by the inflation tax, but had not built up a consumer society. In particular, the reform of the state-owned enterprises dismantled the only safety net that Chinese people knew. The resulting insecurity slowed the development of consumption. Hence, China went into overcapacity-led deflation and depended on export growth to lift the economy out of deflation. After China joined the WTO, it triggered a wave of manufacturing relocation to China. Its efficiency gains fueled strong global growth for the past four years. The current inflation reflects the success of this export-led growth to solve China's overcapacity problem.

Many argue that China's inflation reflects the currency appreciation pressure, i.e., inflation is substituting for appreciation. This is partly true. However, I doubt that appreciation will cure inflation. After hitting 7% inflation rate one year ago, India allowed the currency to appreciate by 10%. Its inflation cooled to 5% but only temporarily. In the 1980s, Japan, Korea, and Taiwan all appreciated their currencies by 30-50% but didn't stop inflation in their economies. Inflation is like a stream that flows. Appreciation is like a dam that stops inflation temporarily. When the dam is filled to the rim, inflation picks up again. Inflation is a sticky variable in an economy. It doesn't move quickly and its momentum is very hard to stop or reverse.

The late great economist, Milton Friedman, once remarked that inflation was a monetary phenomenon. This simple observation is called monetarism. Under an ideal situation, price is equal to the ratio of money over goods and services sold. It is like calculating the depth of a reservoir. Its depth is equal to the ratio of the water volume over the surface area, if we assume the reservoir has straight walls to the bottom. Friedman goes further by arguing that people understand this. This would deny the possibility of monetary stimulus. When a central bank prints money, people would know its consequence for inflation and, hence, demand wage increase today to offset the reduction in the purchasing power of their wage due to the price increase. Businesses also see the situation, accept labor's wage demand, and increase sales price to absorb the cost increase. Hence, monetary stimulus would immediately lead to a general rise in price and input cost in the same portion as the increase of money supply.

However, an economy is far more complicated than a reservoir. Money flows around as companies, financial institutions, households, and governments decide when and how to spend their money. These decisions are driven by all sorts of emotions and desires. Market structure can change from time to time, sometimes due to government actions. It also affects how fast money flows around. Economists quantify such factors in the variable of velocity of money. This velocity of money shouldn't change significantly over time as people usually don't their behavior quickly. Some economists think that the inertia in human behavior opens up the possibility for monetary stimulus. When a central bank prints money, people may not understand the consequence for price and don't demand wage increase. As the extra money creates demand, businesses make more money and hire more people. Wage begins to rise when the labor market is fully employed. Compared to Friedman's scenario, the transmission of money increase into inflation goes thru the labor market and, hence, creates extra economic activities, i.e., stimulus has worked.

The effectiveness of monetary stimulus actually depends on fooling people. Clearly, people can be fooled sometime. There are hundreds of pyramid games in China everyday. Bubble frequently happens in stock or property market. Human nature can be irrational and for an extended period of time. But, learning is another important human characteristic. People cannot be fooled all the time. There is an American saying: 'fool me once, shame on you; fool me twice, shame on me'. It summarizes the importance of learning in human behavior. The history seems to suggest that there is a tipping point in human behavior. People assume the best or worst in viewing the world. When inflation first begins, people try to explain it away by citing temporary factors. As inflation keeps rising, people will switch to believing the permanence of inflation and hoarding durable goods or hard assets to decrease money in hand. Such behavior leads to inflation accelerating. At that point, if government keeps monetary stimulus as money demand is collapsing, it would lead to hyperinflation as what occurred in Germany in the 1920s and in China in the late 1940s. If the government wants to stop inflation, it has to reverse people's expectation by creating a severe recession to convince people of its intention as what the Fed under Paul Volker did in early 1980s.

The past twenty years have given us usual experiences in the linkage between money and inflation. First, the Bank of Japan injected vast amounts of money into its economy after Japan's property bubble burst in 1990s. It didn't lead to inflation. As property price collapsed, Japanese saw the value of money rising and, hence, demanded to hold more and more money, i.e., the household sector didn't spend more in response to monetary stimulus. The collapsing property price also crippled corporate balance sheets and created vast amounts of bad debts for banks. They were not in a position to spend a lot of money either. In the end, the government spent and spent to keep the economy up. Japan's economy has recovered as its businesses and households have been able to make money from the government spending to strengthen their balance sheets. Japan's deflation trap has scared a generation of central bankers. This explains why they were so eager to cut interest rates after the IT bubble burst in 2000 and the '9-11' in 2001.

Second, prolonged loose monetary policy around the world has not caused high inflation in the past six years. Instead, asset prices like property, stocks, bonds, and commodities have kept rising, rising, and rising. But, global inflation remains under 3%, though much higher than 1% at the bottom in 2002. It seems that the linkage between inflation and money supply has broken. Instead, the linkage between asset price and money supply is very strong. It opens up the possibility for central banks to manage their economies through influencing asset prices. When an economy is weak, its central bank can print money to inflate asset prices, which triggers more spending thru the wealth effect. When the economy cools, it can withdraw some money to reverse the process.

The magic of managing demand through asset price is just that, magic, I believe. Two temporary factors have made this possible. First, globalization created fear among labor in the West. As factories moved east, capital had more bargaining power against labor. This downward pressure in labor cost makes wage temporarily insensitive to money supply. However, as the factory relocation completes and displaced workers have found alternative employment, labor market normalizes. In the US, for example, labor cost is rising at the fastest pace in five years despite a sluggish economy.

Third, Wall Street lost its way after the tech burst and wanted profit at any cost. After the tech burst, Wall Street's profit collapsed. Its profit model depended on allocating hot IPO's to institutional investors in return for commission business from them. Without hot IPO's, institutional investors were not willing to pay fat commissions for trading stocks. Hence, both the underwriting and commission income collapsed. In search of new profit source, Wall Street jumped on borrowing money at low interest rate to buy higher return but higher risk assets like emerging market currencies. The successes of the Wall Street firms in this so-called 'carry trade' triggered many imitators like hedge funds. All these people play with other people's money (or 'OPM'). The traders at Wall Street firms bet the money of their companies, would get big bonuses if the trade worked, and, if the trade failed, find another job. Hedge fund managers got 2% management fee and 20% share in profit. Better than the traders at Wall Street firms, they would get rich even if their investors lost money and richer if their investors made money. These people were in paradise.

The OPM phenomenon is the reason for the tight linkage between asset price and monetary policy. As more and more OPM goes into inflating asset prices, bubbles become bigger and bigger. One day, they pop. The credit bubble in the US, for example, is bursting. The losses trigger so much pain among final investors that OPM disappears. That would sever the linkage between money supply and asset price.

Hence, the usual linkages between money supply, inflation, and asset price are due to a shock from globalization and the OPM phenomenon on Wall Street. The former is temporary, and the later a bubble. Both are losing effectiveness. The linkage between money and inflation may get normalized in future, i.e., monetary stimulus leads to inflation, and inflation expectation causes interest rate to rise and asset prices to fall.

The above story on how inflation works and why inflation has behaved differently in past five years doesn't completely explain China's inflation cycle. China is a vast developing economy with a tendency to over-invest. Such a bias creates deflation-inflation cycles. Investment slows only when overcapacity causes price decline and the ensuing profit squeeze decreases the cash available to businesses or governments for investment. The Austrian School of Economics was describing such a dynamic in Western Europe during the 19th century. However, globalization alleviates the severity of this dynamic in the Chinese economy. When Chinese economy suffers from deflationary pressure, the ensuing reduction in cost attracts economic activities from elsewhere, and China's exports grow strongly. This is why export to GDP ratio in China, about 37% for 2007, has a tendency to rise.

During the deflationary period, China's money supply kept rising faster than GDP, i.e., money to GDP ratio kept rising. But, deflationary expectation was increasing demand for money, and the rapid money growth didn't lead to inflation. The switch from deflationary to inflationary expectation is very complicated. The process in this cycle began with the rise of property price. Between 1994-2000, property prices were falling. For example, Shanghai's fell by over 60%. Falling property prices stopped construction. There are still abandoned building sites from that era today. The resulting decline in supply and the rise in demand due to GDP growth finally brought the two in balance. That point was reached in 2000, I believe. The prices then began to rise gradually in line with income growth. The rising trend finally attracted the attention of speculators. Starting in 2003, the price began to rise sharply in Shanghai, spread to Beijing and Shenzhen in 2005, and finally to most provincial capital cities now.

Property price is the most important driver for inflation expectation. Even though it is not in the CPI, household expenditure on property would average 25-30% of household income over a lifetime and is bigger than on food in a middle class society. China is transiting towards a middle-class society. The importance of property price in inflation expectation is just beginning.

Second, the global economic boom has triggered sharp increase in the prices of raw materials. The Commodity Research Board ('CRB') index has roughly doubled from the bottom in 2002. Its inflationary effect through cost push is still ongoing. For example, high oil price has led the US government to support bio fuel through policy subsidy. It triggered doubling of corn price and inflation of agricultural commodities in general. The rising price of feedstock made pig farming unprofitable in China. When many farmers abandoned pig farming, pork price rose sharply. The rise in pork price will force price increase in downstream products like sausage.

One may argue that the cost-push inflation is temporary. When the higher costs of raw materials are fully absorbed, the inflation should stop. But, the trend changes inflation expectation, and people become more willing to spend and to accept price increase. When money supply is already very high due to past deflation, it can lead to sustained inflationary trend.

Third, stock market followed property market and began to rise sharply in 2005. Liquidity doesn't automatically lead to asset bubble. The combination of optimism and liquidity lead to bubble. As relocation of manufacturing to China powered the economy forward, the 2008 Olympics got closer, and currency appreciation expectation strengthened, popular expectation became more and more bullish. The sentiment finally increased demand for shares. Like property, the uptrend in the stock market attracted speculators and turned from a bull market to a bubble market quickly.

As people see rising prices of property, stocks, and more and more products, they begin to accept price increase. This is equivalent to a reduction in price sensitivity in demand. Businesses suddenly realize that they can increase prices without sacrificing sales like before, i.e., the fear of price competition diminishes. Cutthroat price competition severely scared Chinese businesses in their psychology. Their knee jerk reaction to any problem is to cut price. They then try to cut costs to survive. However, the increasing trends in the prices of raw materials and wages have cornered them. They have been trying to cut costs by downgrading materials or portions. The recent spate of quality problems may stem from that behavior. The only solution is to raise prices. The change in demand dynamic also allows price increase to stick. This is why inflation in China is just beginning.

There are two arguments against inflation. First, China still has overcapacity. The overcapacity problem is much less than what statistics suggest. China is developing so fast that past capacities may become obsolete quickly. For example, automobile industry has massive overcapacity and the prices of some automobiles keep falling. However, demand is shifting to higher quality cars. Camry, for example, has a long waitlist for over a year. In restaurant business, demand is upgrading very fast. Traditional restaurants are experiencing demand weakness, while modernized ones have long queues. Demand upgrading is a major reason that statistical overcapacity doesn't mean the same at different times. One must look at the demand dynamic for a better judgment.

Second, China still has excess labor supply, and wage should stay sluggish to stop the dangerous wage-price spiral. Some analysts have argued that China doesn't have excess labor anymore. I am not in that camp. China's urbanization is only 43%. It is hard to believe that labor surplus is exhausted at such an early stage of urbanization. But, labor surplus doesn't mean that wages cannot rise. First, when living cost rises in an inflationary environment, businesses need to keep wages rising in tandem. Otherwise, workers may feel cheated and work away. The social pressure or human desire for dignity prevents real wages from declining in a modern society. Second, experience is a bottleneck in China's labor market due to the rapid economic expansion. Wages in this part of the labor market are under enormous upward pressure. The compensation for senior managers is reaching international levels. Third, China's service sector is strong enough to compete for labor against the manufacturing sector. The labor shortage in the export sector is due to this force. The modernization of the service sector requires new type of labor skill. Only youth can be trained easily to fill the jobs in this sector, the same as the export factories. The 'labor shortage' in the export sector actually reflects that its wages are below market level. Hence, wages in China have another big leg up.

Inflation is a supertanker. When it gets going, it is hard to stop. Supply-demand dynamic, labor market balance, and demand psychology are suggesting that China has entered the era of inflation and it may last for many years. Frankly, it is too late for China to take actions to stuff inflation back in the bottle. What China can do is to slow its rise and prevent too much excess building up during the process.

China's inflation may be heading to 7% sometime in 2008. 7% is not usual for developing countries during high economic growth. India is seeing it now. Southeast Asia and Korea saw similar levels of inflation ten years ago. The top priority is to slow inflation expectation. If expectation of rising inflation becomes entrenched, dynamics in labor, product, and service markets could get into a vicious spiral, which would force drastic tightening and a hard landing for the economy.

To stabilize inflation expectation, the government must (1) introduce tightening steps to show that it wants to contain inflation and (2) cool asset inflation that inflames inflation expectation. Interest rate, for example, must be increased much more in the next 18 months. And, the government should try to increase interest rate faster than inflation. Otherwise, monetary policy is not tightening. China needs to raise interest rate by 200 bps over the next 18 months at least. 300 bps may be necessary. The past pace of rate increase is too slow. When people think that the government is not sincere about tightening, inflation expectation could run amok.

Asset inflation serves to inflame inflation expectation and increases demand that boosts inflation also. The past cooling measures, though have served some propaganda purposes, have not been very effective. Both property and stock markets are accelerating in the past three months. Asset inflation fuels the belief that money is depreciating in value. One byproduct is increased willingness to accept price increase. I believe that, to contain inflation expectation, China has to stop and reverse the rise of property price. Average ratio of new property value and household income is already around 15 for many cities. When price rises by 10%, it is equivalent to 1.5 times household income, which creates an intense feeling of money depreciating and prepares consumers to accept inflation. To cool inflation, China must cool property market first. If inflation expectation runs out of control, a hard landing may become inevitable.

Excesses can build up during inflation and, when a shock hits the economy, causes a hard landing. The most likely candidate is a debt bubble. When inflation is high, it usually leads to low real interest rate and creates two important effects. First, real interest rate tends to be low during high inflation. Hence, businesses are more willing to borrow. In particular, they want to borrow to buy appreciating assets like land. Virtually every debt bubble happens during high inflation and is for financing property acquisition. Something similar is already happening. On the household side, it is not yet so serious. Mortgage debt outstanding is about Yuan 3 trillion or 8% of GDP. The magnitude is not yet big enough to threaten economic stability. But, the debt for holding land banks by property developers is hard to estimate. The official data on banking property exposure probably underestimates the true exposure. Many traditional businesses have expanded into property in the past three years. The banks may not have classified their debts as belonging to the property sector.

The National Bureau of Land and National Resources have repeatedly stated that the land sold is equal to many years of demand. Such land holdings must be financed by bank loans. The land hoarding decreases property supply in the short term, which inflates property price, and ties down vast amounts of loans. When land prices reverse, the loans may turn bad and cause a banking crisis. This is, I believe, the weakest point in China's economy today. If the government does not rein in the speculative mania in land market, it would certainly lead to a banking crisis, though it may take many years to come.

Second, business profit rises rapidly. China's business debt is about Yuan 20 trillion. The real interest rate has declined by about 4 percentage points in the past five years. That implies Yuan 800 billion less interest payment. This reduction in debt burst has been the main driver for corporate profits over the past five years. Rising profitability makes businesses more willing to expand. As the high profitability is due to inflation-a temporary factor, businesses are misled into overexpansion, which leads to a capex bubble. It happened in Japan during 1980s and Korea during 1990s. The capex bubble eventually leads to bad loans also. When the bubble bursts, businesses have to cut prices to sell enough. The reduced revenues may not be able to service loans.

The National Development and Reform Commission (the 'NDRC') is the gatekeeper in preventing overcapacity. Any significant project has to receive its approval. But, we need to be careful about relying on bureaucracy to predict demand. A better solution is to use market force. China's banks should be trained to assess long-term business prospects in their lending decisions. Sound banking practice is the most important weapon in the fight against overinvestment and financial crisis.

In summary, China has entered the inflation era. The main macro objectives are to prevent hard landing and financial crisis. The main tools are (1) sustained tightening to contain inflation expectation and (2) controlling debt increase for land hoarding and excessive capex.

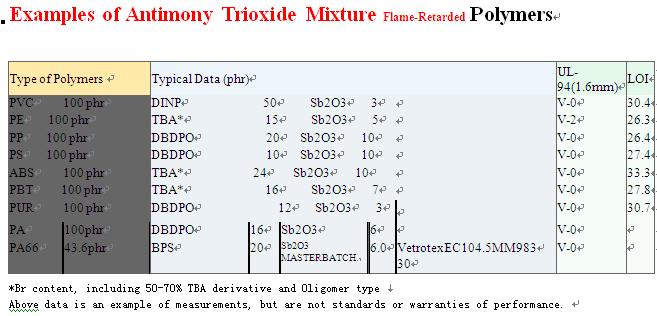

We can supply any quantity and any kind of Antimony products and fire retardant from stock.would you please inform us how many you need and your target price, then we will confirm ASAP. We are sincerely hope to do business with you and establish long term business relationship with your respectable company.

Look forward to hearing from you soon.

Best regards,

Sam Xu

MSN: xubiao_1996@hotmail.com

GMAIL: samjiefu@gmail.com

SKPYE:jiefu1996

Fire retardant masterbatch

0 comment:

Post a Comment